TL;DR:

- Crypto investors in the EU must fully disclose all crypto gains, income, and activities to comply with evolving reporting laws. Nearly all crypto transactions, including swaps, staking rewards, and airdrops, are taxable events, requiring diligent record-keeping and timely reporting. Utilizing dedicated tax tools and maintaining consistent records simplifies compliance and reduces audit risks, transforming tax reporting into an integrated part of investment management.

Crypto investing in the EU carries a legal responsibility that many investors underestimate. The idea that small or anonymous transactions quietly “fly under the radar” is one of the most persistent myths in the space, and tax authorities across Europe are actively working to prove it wrong. With new data-sharing frameworks tightening reporting requirements every year, every EU investor needs to understand what crypto tax reporting means, which activities trigger obligations, and how to file correctly. This guide cuts through the noise and gives you a clear, practical path forward.

Table of Contents

- Understanding crypto tax reporting in the EU

- Which crypto activities are taxed?

- How to report your crypto taxes: step-by-step process

- Common mistakes and how to avoid them

- Why most crypto investors overcomplicate tax reporting

- Streamline your crypto tax reporting with CryptoCracker

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Crypto taxes are mandatory | EU investors must report relevant crypto transactions to tax authorities every year. |

| Know what triggers tax | Even small trades, airdrops, or staking rewards can create tax events that require reporting. |

| Keep detailed records | Accurate transaction logs and supporting documents simplify compliance and help avoid costly mistakes. |

| Use effective tools | Automated tracking and reporting software reduce effort and minimize audit risk for crypto holders. |

Understanding crypto tax reporting in the EU

Crypto tax reporting means declaring any gains, losses, or income generated from cryptocurrency activities to your country’s tax authority. It is not a gray area. Across EU member states, tax authorities treat crypto assets as taxable property or financial instruments, and the expectation is full, accurate disclosure.

The regulatory environment has shifted significantly. The EU’s global crypto regulations framework, including the Markets in Crypto-Assets Regulation (MiCA) and the DAC8 directive, now requires crypto service providers to share user transaction data directly with tax authorities. That means exchanges and platforms operating in the EU are legally obligated to report your activity. You cannot rely on anonymity.

“Crypto assets are no longer a shadow market. EU tax authorities now have the tools, the mandates, and the data to track gains and enforce compliance, regardless of transaction size.”

Here is a snapshot of how major EU countries treat crypto for tax purposes:

| Country | Tax treatment | Rate |

|---|---|---|

| Germany | Tax-free after 1 year holding | 0% after 1 year; up to 45% if sold sooner |

| France | Flat tax on crypto gains | 30% flat rate (PFU) |

| Spain | Capital gains tax on all disposals | 19% to 28% depending on gains |

| Ireland | Capital gains tax | 33% on gains above annual exemption |

| Netherlands | Deemed yield on crypto wealth | Box 3 wealth tax, varying rates |

Each country has its own rules, deadlines, and filing systems. What they share is a growing expectation of transparency. Even if you only made a few trades last year, your transactions may already be visible to your local tax office through automated reporting.

Key regulatory drivers shaping EU crypto tax reporting today include:

- DAC8: Requires EU-based crypto service providers to report client data to tax authorities starting from 2026

- MiCA: Sets consistent rules for crypto markets across the EU, improving oversight

- OECD CARF: A global crypto asset reporting framework that many EU countries are adopting

- AML Regulations: Anti-money laundering rules that enforce identity verification on platforms

Understanding this landscape is the foundation. Everything else builds from here.

Which crypto activities are taxed?

With a broad view of crypto tax reporting in place, it is essential to know which transactions actually trigger tax obligations. Many investors assume only direct crypto-to-fiat sales count. The reality is much broader, and some of the most commonly overlooked triggers catch investors off guard during tax season.

Here is a breakdown of taxable versus non-taxable activities across most EU jurisdictions:

| Activity | Taxable? | Notes |

|---|---|---|

| Selling crypto for fiat | Yes | Triggers capital gains tax |

| Crypto-to-crypto swap | Yes | Treated as a disposal in most EU countries |

| Staking rewards received | Yes | Taxed as income when received |

| Mining income | Yes | Taxed as income at fair market value |

| Airdrop tokens received | Yes (usually) | Treated as income in most countries |

| Buying crypto with fiat | No | Not a taxable event itself |

| Holding crypto long-term | No | Until disposal occurs |

| Transferring between your own wallets | No | Not a disposal event |

| Receiving crypto as a gift | Varies | Country-specific rules apply |

The step-by-step guide to crypto taxes explains each of these categories in detail, but let us focus on a few hidden triggers worth highlighting.

Crypto-to-crypto swaps are one of the most commonly missed tax events. Swapping Bitcoin for Ethereum, for example, is treated as selling Bitcoin at its current market value. Any gain from your original purchase price to the swap price is taxable. Many investors do this dozens of times without realizing they are creating taxable events each time.

Staking rewards are another grey area that is rapidly becoming clearer. Most EU tax authorities now treat staking income as ordinary income, taxable at the time you receive the rewards, not when you later sell them. This means your staking yield is effectively taxed twice if you later sell at a gain.

Airdrops are similarly complex. Receiving free tokens may feel like a windfall, but tax authorities generally view them as income equal to the market value at the time of receipt. If those tokens later increase in value, you will also owe capital gains tax when you sell.

Following crypto investing best practices from the start, including keeping detailed records of every transaction, the date, the asset amount, and the market value at the time, protects you from scrambling at year-end.

Pro Tip: Use a dedicated spreadsheet or crypto tax tool to log every transaction the moment it happens. Reconstructing months of activity later is far harder than recording it in real time, especially for DeFi and staking activities where on-chain data can be difficult to interpret retroactively.

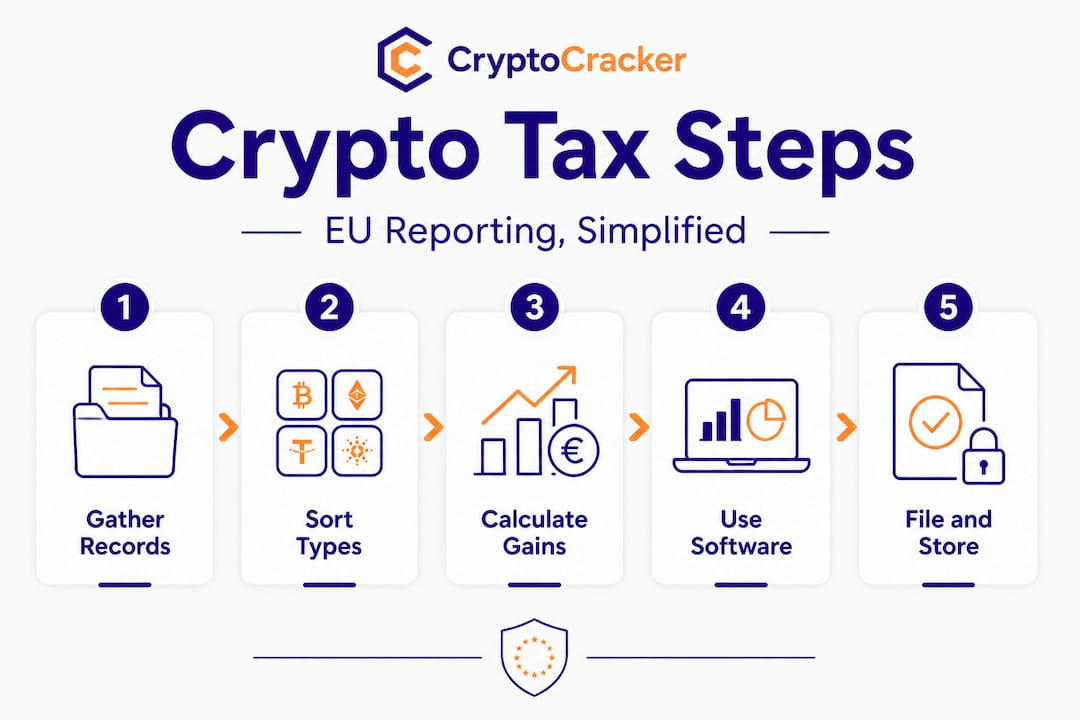

How to report your crypto taxes: step-by-step process

Knowing which activities are taxed makes the reporting process much more approachable. Let us break it down into clear, manageable steps that any EU investor can follow, whether you made five trades or five hundred.

Step 1: Collect all your transaction histories

Start by downloading your complete transaction history from every exchange, wallet, and platform you used during the tax year. This includes centralized exchanges like Coinbase, decentralized exchanges (DEXs), and any DeFi protocols. Many platforms provide downloadable CSV files. If you used multiple wallets, include all of them.

Step 2: Organize transactions by type and date

Sort your transactions into categories: buys, sells, swaps, staking income, mining income, airdrops, and transfers. For each taxable event, you need the date, the asset, the amount, the value in euros at the time, and the original purchase price (known as your cost basis).

Step 3: Calculate your gains, losses, and taxable income

For each disposal, subtract your cost basis from the sale price to find your gain or loss. Each EU country uses slightly different methods for calculating cost basis, such as FIFO (first in, first out) or average cost. Check your local tax authority’s preferred method. Sum up all taxable income from staking, mining, and airdrops separately.

Step 4: Use compliant reporting tools

Manually calculating gains across hundreds of transactions is error-prone. Dedicated crypto tax software can automate most of this, connecting to your exchanges and wallets to pull data automatically. If you want to track crypto portfolio performance and tax obligations in one place, purpose-built platforms save significant time. For Irish investors specifically, crypto tools for Irish investors offer country-specific compliance features aligned with Revenue rules.

Step 5: File your report with your local tax authority

Each EU country has its own filing system and deadlines. In Germany, you file via your annual income tax return (Einkommensteuererklärung). In France, you use Form 2086. In Ireland, you file a Capital Gains Tax return with Revenue. Always double-check the current year’s deadline and required forms directly from your country’s official tax authority website.

Step 6: Keep records for at least five years

Most EU tax authorities can audit up to five years back. Store your transaction records, tax calculations, and filed reports securely for at least that long.

Interestingly, automated tax software adoption is growing fast among EU investors, with adoption among active crypto investors in Europe estimated to be growing at over 40% year-on-year as compliance pressure increases. Automation removes calculation errors, reduces time spent, and creates an audit-ready record.

Pro Tip: Schedule a quarterly portfolio review to check for taxable events you might have forgotten. Catching these every three months is far less stressful than a full year’s reconstruction in April.

Common mistakes and how to avoid them

Armed with the reporting process, it is equally important to recognize the pitfalls that trip up even experienced investors. These mistakes are more common than you might think, and they can result in penalties, audits, or overpayment.

1. Ignoring small transactions

Many investors assume that small trades or micro-transactions are not worth reporting. Every taxable event matters, regardless of the euro amount. Tax authorities aggregate all your transactions, and small omissions add up. Report everything.

2. Skipping crypto-to-crypto trades

This is the single most common mistake. A Bitcoin-to-Ethereum swap, a swap on a DEX, or even converting crypto to a stablecoin are all taxable disposals in most EU countries. Treat every swap as if you sold for euros first.

3. Forgetting staking, mining, and airdrop income

These are income events, not capital gains events. They need to be reported in the year you received them, even if you never converted them to fiat. Missing these creates discrepancies that can trigger an audit.

4. Poor record-keeping or lost data

If an exchange closes, if you lose access to a wallet, or if a platform deletes historical data, reconstructing your transaction history becomes a nightmare. Backup your data regularly.

5. Submitting without reviewing

Rushing to file at the last minute often leads to errors. Always review your calculations before submitting, ideally with fresh eyes or a second check from a tool.

To avoid all of these, we recommend setting calendar reminders at the end of each quarter to review and log your transactions. Use secure crypto trading practices not just to protect your assets, but also to maintain the clean data trail that makes tax compliance straightforward.

Pro Tip: Store copies of your transaction records in at least two secure locations, such as an encrypted cloud backup and a local external drive. If one source fails, you still have a complete audit trail ready to go.

Why most crypto investors overcomplicate tax reporting

Finally, let us address the real issue: why does crypto tax reporting feel so overwhelming to so many people, even experienced investors?

We think the honest answer is that the anxiety is often bigger than the actual complexity. Most investors have far fewer taxable events than they think. And the ones who do have complex portfolios, staking positions, or DeFi activity can manage compliance systematically if they build the right habits early.

The conventional wisdom says “crypto taxes are complicated, so hire an expensive accountant and hope for the best.” We disagree. While professional advice is valuable for genuinely complex situations, the majority of EU crypto investors can handle their own reporting with the right tools and a methodical approach. The key is treating tax reporting as part of your investment discipline, not as a separate, dreaded annual event.

Think of it this way: you check your portfolio’s performance regularly. You track gains and losses in real time. Tax reporting is simply the formal extension of that same habit. When you approach reducing crypto tax risk the same way you approach managing investment risk, it becomes a natural rhythm rather than a once-a-year scramble.

The investors who struggle most are those who trade frequently, never record anything, and then try to reconstruct a year of activity in a single weekend. The investors who handle it smoothly are those who log transactions as they happen, review quarterly, and file using tools that do the heavy calculations automatically. The difference is not intelligence or financial expertise. It is consistency.

We believe the mindset shift from “I have to do my crypto taxes” to “I maintain my financial records accurately” is the single most powerful change any investor can make.

Streamline your crypto tax reporting with CryptoCracker

Staying on top of crypto tax obligations does not have to be a stressful process. At CryptoCracker, we have built a platform that makes managing your crypto portfolio and staying compliant feel like two sides of the same coin.

Whether you are just starting out or managing a diverse portfolio across multiple assets, our tools give you real-time visibility into your transaction history, gains, and tax-relevant events. Explore our complete guide to crypto investment to build a strong foundation, and then use our crypto management tools to keep your records organized and your reporting ready. We make it practical, secure, and designed specifically for EU investors who want clarity without complexity.

Frequently asked questions

Do I need to report every small crypto transaction in the EU?

Yes, all taxable events must be reported regardless of transaction size, because EU regulations require complete and accurate disclosure of all crypto gains and income.

What happens if I fail to report crypto gains in the EU?

Failure to report can lead to financial penalties, tax authority audits, and back taxes owed, with interest added in many EU jurisdictions.

Are crypto-to-crypto trades taxable in most EU countries?

Yes, most EU countries treat crypto-to-crypto trades as disposals that may trigger capital gains tax, even if no fiat currency was ever received.

Can I use crypto tax reporting software to simplify the process?

Yes, automated crypto tax tools can connect directly to your exchanges and wallets, making it significantly easier to track, calculate, and submit accurate reports on time.

Recommended

- How to Manage Crypto Taxes: A Step-by-Step Guide for EU Investors | CryptoCracker

- Crypto management for Irish investors: tools and tax 2026 | CryptoCracker

- Simplified crypto trading explained: easy strategies in 2026 | CryptoCracker

- Global cryptocurrency regulations list: investor essentials | CryptoCracker